(Iraqi Oil Minister Jabar al-Luaibi (C) attends the Iraqi oil and gas exploration and development contract auction in Baghdad, Iraq April 26, 2018. Reuters/Khalid al-Mousily)

A lot of inaccurate articles and reports have been written about the new oil and gas licensing round that was recently held by the Ministry of Oil in Iraq, which led to ambiguity amongst many observers. This article aims to clarify a few points about the new licensing round especially given claims that it was not in favor of Iraq.

In order to do an accurate fiscal evaluation of the latest licensing round we must analyze the contracts based on their essential elements.

First, using service contracts by the Iraqi government alone is considered an advantage. In comparison, concessions contracts the investor owns all explored oil whether in the reservoir or extracted and pays a royalty and taxes to the host government, whereas in the production sharing contracts the investor owns only a share of the extracted oil. However, in service contracts the investor is not entitled to any ownership related to the oil, just remunerations.

Second, the Iraqi government did a clever blend between its service contracts that give the entire ownership to the government and production sharing contracts that have a simple fiscal framework to achieve the advantages of both types. In other words, the contractor’s remuneration was set with a fixed amount of dollars per barrel according to R Factor. R Factor is a formula used in oil contract with the purpose to prevent the accumulation of excessive benefit of the investing company. Based on R factor, the more the production increases, the less the return of dollars per barrel becomes. The new fiscal framework that is used in the fifth licensing round is closer to the production sharing fiscal framework which links the profit of the investor to the overall revenue of the project as fixed percentage.

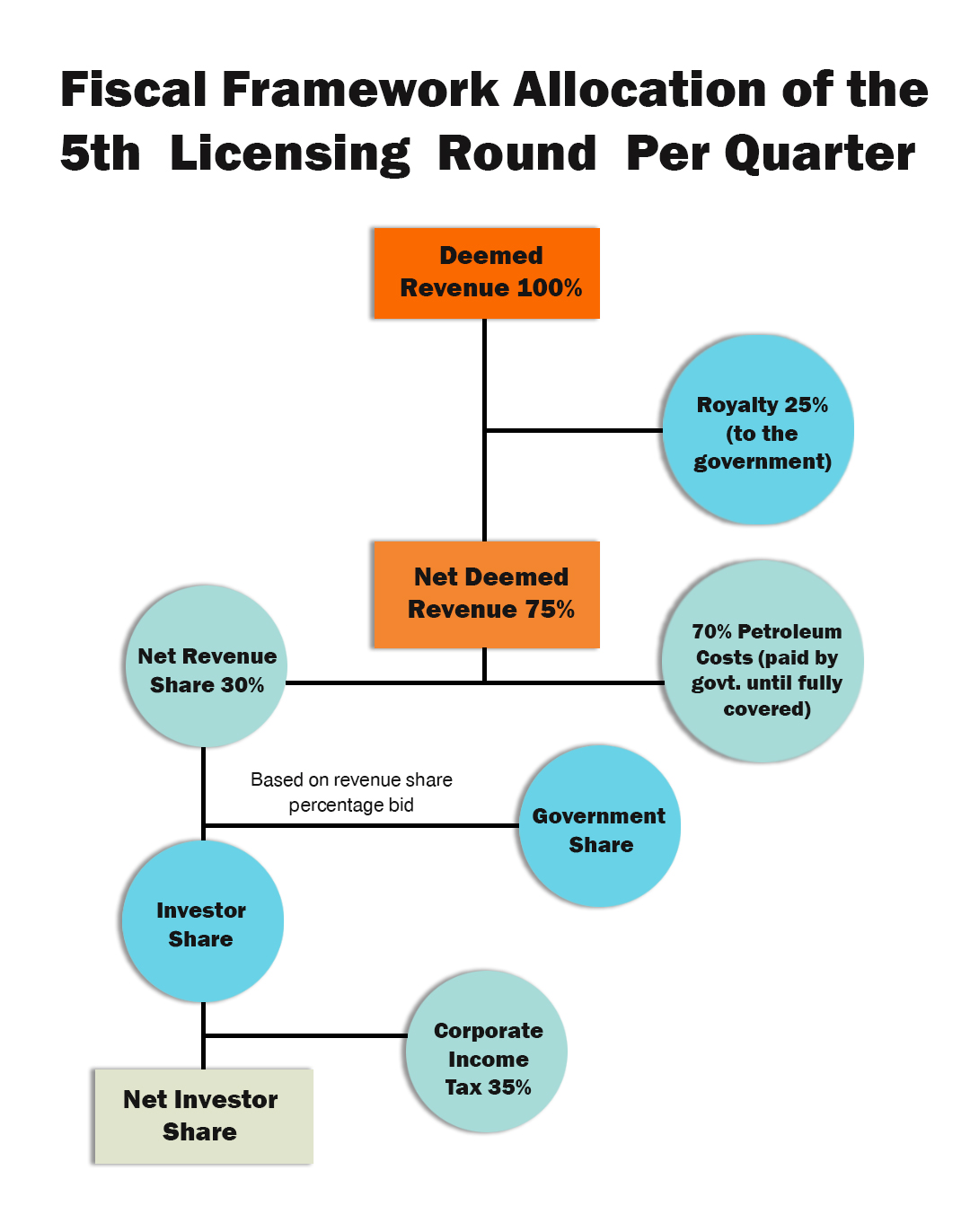

In accordance with article 19 of both contracts utilized in the fifth auction round, which illustrates the fiscal framework, Iraq’s involved regional oil company (ROC), in any quarter, shall be entitled to a royalty of 25% of the deemed revenue. Therefore, the contractor will recover the petroleum costs according to the oil sale price. If the price is equal to or less than $21.50 per barrel, the amounts that shall be allocated for the repayment of the petroleum costs (the costs of the oil project) shall be 30% of the net deemed revenue (the remaining revenue after deduction of royalty). Where the average oil sale price is equal to or greater than $50.00 per barrel, the amounts that shall be allocated for the repayment of the petroleum costs shall be 70% of net deemed revenue.

The contract will then split the remaining net revenue share with the government according to the percentage established at the time of the bidding round.

These are the remuneration percentage bids according to the six awarded blocks:

- Khashim Ahmer-Injana (gas, Diyala Governorate): 19.99%, Crescent Petroleum

- Naft Khana (oil and gas, Diyala Governorate): 14.67%, Geo-Jade

- Khider al-Mai (oil, Basra Governorate): 13.75%, Crescent Petroleum

- Gilabat-Qumar (gas, Diyala Governorate): 9.21%, Crescent Petroleum

- Huwaiza (oil, Missan Governorate): 7.15%, Geo-Jade

- Sindabad (oil, Basra Governorate): 4.55%, United Energy Group.

Finally, the investor will pay the 35% corporate income tax on their percentage of net revenue share.

Third, in accordance to the oil price studies of recent years and the forecasts of future oil prices it is unlikely that the price of oil will drop to $21.50 per barrel. Therefore, the 70% of the deemed revenue after deducting the royalty (which is called net deemed revenue and goes to the government) will be allocated for repayment of petroleum costs. As mentioned above, these represent the costs of the oil project in question. These include exploration activities, drilling, buildings related to the projects, pipelines and other infrastructure related the project. A lot of these costs actually return to the government, because these infrastructures will become Iraqis assets the moment they are built or enter Iraqi soil based on the contract. On the other hand, the high petroleum costs repayment rate embodies the Iraqi government policy of attracting foreign investors to develop the oil and gas sector in Iraq, because this will speed up the repayment of said amounts and subsequently the investors will be able to invest and obtain the benefits in other places in the world.

Fourth, some have claimed that the issue of petroleum costs is vague. Based on the type of contract utilized by Iraq, after the end of the repayment of the full petroleum costs by the government, the later obviously will stop paying these. If there would have been a partnership between the government and the investor, anything beyond the petroleum costs would be divided between the two. However, according to the current contract (article 24), there is no partnership between the investor and the government, and hence the state owns everything after paying the petroleum cost.

To conclude, these new contracts will bring lots of benefits to Iraq. From a fiscal perspective, the profitability for Iraq will be relatively higher than the production sharing contracts utilized in United Arab Emirates and Kurdistan Region of Iraq. At the same time it will provide reasonable profitability and other incentives for foreign companies to invest in the Iraqi oil and gas sector.

Youssef Ali

Youssef Ali is a Ph.D researcher in international law. He specializes in international oil and gas law and is interested in Iraqi political and legal affairs.